Market Commentary - March 2021

South Africa Markets

The South African Economy contracted by 7% in 2020, this is better than 7.4% to 11.5% contraction forecasted earlier in 2020. The Eskom blackouts are a major threat to the speedy recovery of the economy i.

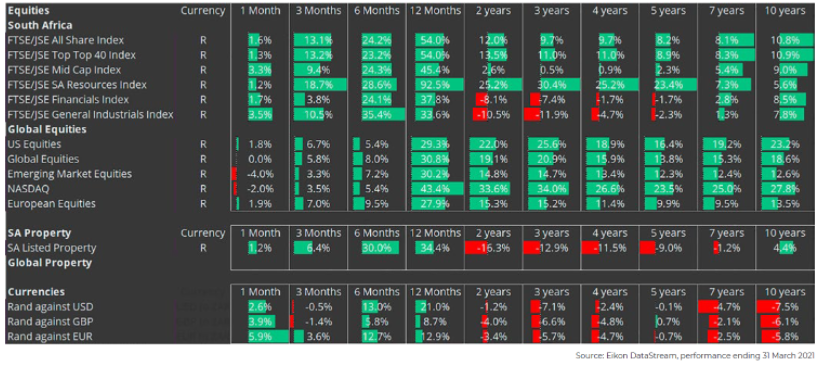

Inflation is still under control, the headline inflation was 2.9% in February from 3.2% in January. It is the 3rd time in 12 months that CPI is below the SARB target range ii. The Rand continue to hold its ground against major currencies, the Rand gained 21% against the greenback, 12% against the Pound and 5% against the Euro for the year ending 31st March 2021, and the Rand has been flat against major currencies for the past 5 years.

The Rand is one of the few Emerging Markets currencies which has gained against the US Dollar in the first quarter of 2021. The South African Equity market had a good first quarter, the broader index gained more than 13% year to date, and this was attributed by strong performance in resources sector iii. The resources index has gained close 20% for the quarter and almost 100% for the year. The high Iron ore and PGM prices have helped have helped commodity producing companies in posting strong earnings.

The rising US yields left South African fixed income less attractive, South African Sovereign bonds posted a 2.6% negative return, Inflation linked bonds were just up by 0.5% for the month of March, however South African fixed income has performed very well for the year iv.

US Markets

President Biden announced a 2 trillion dollar infrastructure program, named “American Jobs Plan” which plans to upgrade US highways, airports and waterway v. The plan is expected to funded by corporate tax hikes, President Biden plans to hike the US corporate tax from 21% to 28%, this is expected to get a pushback from the Republican benches because it is believed that a tax hike will make US companies less competitive.

The US has administered more than 150 million doses of COVID vaccine, with nearly 55 million people fully vaccinated vi. Nonfarm payrolls rose 916 000 in March, which is defined as employment in the formal sector vii. Which led the unemployment rate to decline to 6% vii.

The S&P 500 index gained 4.24%, bringing its year to date performance to 5.77%, utilities and in the star performers gaining 10.13% and 8.82% respectively for the month viii. The US markets have performed extremely well in the past 12 months ix. The expected 7% GDP growth in the US has pushed the 10 year US Treasury yields up nearly 1%, to nearly 2%, still at low levels relative to history.

With interest rates being low and Congress passing a huge stimulus program, this might give rise to inflation and pushing the yield even higher.

European Markets

Germany and France are experiencing a third wave of COVID infections, this has led the two nations to introduce stricter restrictions xi. According to the WHO, the European vaccination program is extremely slow.

European equities had a good March, the German DAX30 gained 8.86%, and the DAX was driven by automakers VW, BMW and Daimler which posted 37.96%, 23.59% and 14.45% respectively xii.

The French CAC40 gained 6.38% for the month of March, the gain was driven by Financials, BNP Paribas and Credit Agricole gained 5.28% and 6.37% respectively. The broader European index the EuroStoxx 600 gained 6.08% in March. The 10-Year Gilt gained 63 basis points leaving the yield at 0.83%.

UK Gilt have delivered a -7.24% for the past 3 months, this might be ca program is starting to gain momentum and things could go back to normality, and investors are moving money into more riskier assets.

Emerging Markets

xiii The MSCI emerging markets was up 2.3% for the month of March. Europe, the Middle East, Africa gained the most at 8.1% this was led Russian Market which benefited from rising oil prices, Latin fact the region is still dealing with COVID outbreaks and lack of vaccine supplies xiv.

The Chinese market was the laggard in Q1 of 2021, as the CSI 300 index of Shenzhen and Shanghai listed shares lost more than 5 percent in value in the first quarter of 2021, the recent regulatory crackdown on ecommerce and Fintech on companies such as ANT financials and Alibaba which was fined $2.8 billion in an anti-monopoly probe, had a negative impact on investor sentiment xv.

The Turkish Lira lost about 11% against the US Dollar was one of the worst performing emerging markets currencies, this is the worst level since 2018, and this was due to the Turkish government interfering in country’s Monetary Policy. By contrast, the rand has gained 21% against the US dollar in the past year.

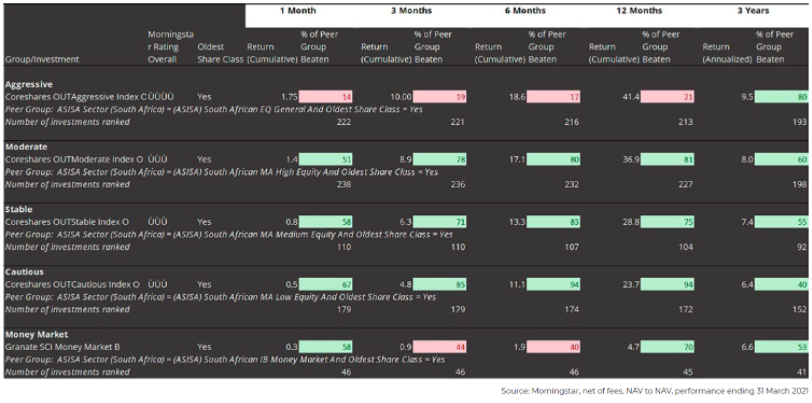

Outvest Funds

Our funds performed satisfactory in the month of March. The gearbox (relationship between risk and return) worked well in the month of March with the highest risk fund – the OUTaggressive fund – returning the highest absolute return out of all our funds.

Our funds have benefited from the strong market recovery in past year, 4 out of 5 of our funds had an absolute return of above 20%, with the OUTaggressive fund returning 41% for the year. The OUTaggressive is the only fund which performed poorly relative to its peers in the past year.

All our funds managed to achieve their respective inflation-linked return targets, on a 3 year rolling basis, ending March 2021.