South African Market

South Africa seems to be in the midst of the third wave. 7-day average new infections are close to 4000 as compared to just 1100 for the same time in the previous monthi.

South Africa administered just under a million doses by the end of Mayii, minister of health Dr Zweli Mkhize expects the vaccination program to pick up pace in the coming weeks with a strong partnership forming between the public and private sector.

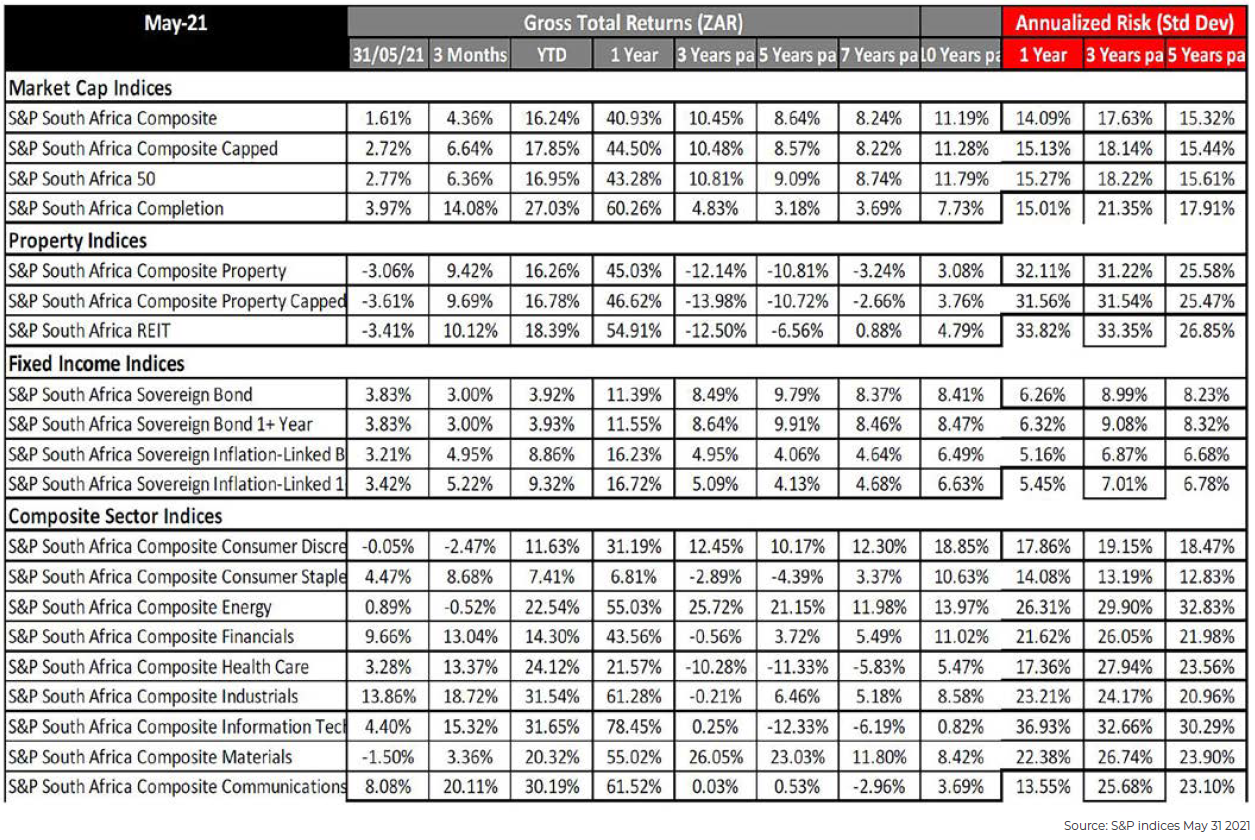

The South African Rand continued its gains into May, the Rand breached the 13.80 mark against the US Dollar, the demand for South African debt and commodity boom can be attributed to the strengthening of the Rand.

South Africa’s Trade Balance (imports vs exports) posted a surplus of 51 billion Rands in the month of April, the March number, at 52 billion is the biggest trade surplus since records beganiii. If continued the trade surplus can support the local currency going forward.

The South African Reserve Bank monetary policy committee kept rates on hold in the May meeting, the Bank forecasts inflation to be 4% in 2021 and 4.2% for the following year. iv

The cutting cycle seems to be over as global inflation starts to pick up. The reserve bank upgraded its GDP forecast for 2021 to 4.2% from 3.8%, the stronger growth forecast reflects better sectoral growth performance and robust trade balance in the first quarter of 2021.

The unemployment rate in South Africa hit an all-time high in the first quarter of 2021 with the official number sitting at 32.6%, meaning that more than 7.2 million people are without jobsv . The more concerning number is the youth unemployment of 74.4%, meaning 3 in 4 persons between the ages of 24 and 15 are not working nor in school, this might cause social unrest and political instability.

South African equities continue to have a good year, the big cap S&P top 50 was up nearly 3% in the month of May. The star performers were the industrial, financial and communication sectors. The sectors were up by 14%, 10% and 8% respectively.

The property sector retracted its gains for the year. All the property major indices were down more than 3% in May, this might be caused by investors taking profits after a strong run.

After a tough year South African fixed income had a good May, both inflation linked-bonds and Sovereign Bonds were up more than 3% in May, with South African Bonds offering an attractive yield in a negative yield environment, our bonds are very attractive for investors who are looking for a better yield.

US Markets

US corporate earnings came in better than expected. The S&P 500 reported earnings growth of 47 % (y/y) with the street forecasting a 20% earnings jump.

This clearly shows that the biggest economy in the world is recovering faster than expected. And this could feed into more attractive valuations potentially providing further upside to markets.

With the big stimulus programs and rates near 0%, US inflation came in above the market expectation, the headline number was 4.2% in April, and this might be transitory considering the prices are coming from a low due to last year’s collapse in prices.

In the April Fed’s minutes the central bank acknowledge that it will need to relook tapering its bonds purchases.

With rising inflation threat, this might be the end of the road of the Fed’s cutting frenzy and rising rates can be expected sooner.vi

The US broader market S&P 500 posted modest gains of 0.7% in the month of May, the sectors with a traditional high PE e.g. Technology and Consumer discretionary which make 40% of the broader market were under pressure due to the rise of inflationary environmentvii.

Due to higher crude prices the energy stocks had a good May with gains of more than 5%.viii

All US fixed income were modest up in May.ix Excluding cash (3-month Treasuries), which remained flat, the weakest performer last month: US junk bonds.

The iBoxx Liquid High Yield Bond Index edged up 0.2% in May. That’s a relatively tepid performance, but keep in mind that this benchmark has enjoyed eight straight monthly gains.x

European Markets

The European vaccination program seem to have caught steam, with nearly 1% of the population vaccinated every day in major economies, this fueled hopes of an economic rebound this year, this optimism carried over into the equity markets.

The European markets EX-UK was the best performing major market in May, with gains of 2.7%.xi

The manufacturing sector also had a positive month, the European PMI hit a 3 year high, and the Purchasing Managers Index was 56.9 for May and 53.8 for April, the manufacturing sector is a leading indicator to a strong recovery.

Less strict restriction in the UK boosted consumer confidence, retail sales the UK in April jumped more than 9%, this is double the average projection in a Reuter’s poll.xii

European Fixed income continue to have an underwhelming year, with most of the fixed income indices in the red for 2021.

European yields continued to rise initially, with the vaccine roll-out and economic recovery gaining traction, then fell in the last week of May on dovish comments from the ECB.xiii

Emerging Markets

Emerging Market equities had a good month with the broader S&P Emerging BMI posting gains of 2.58%, The Hungarian Market was the leader with gains of more than 15%, major emerging market economies Russia and Brazil also had a good month with gains of 9% respectively. xiv

The Chinese growth shares has lost 20% of their value since February, due to fears of regulatory crackdown on major corporations, the valuation of Chinese shares looks attractive.xv

OUT- Funds

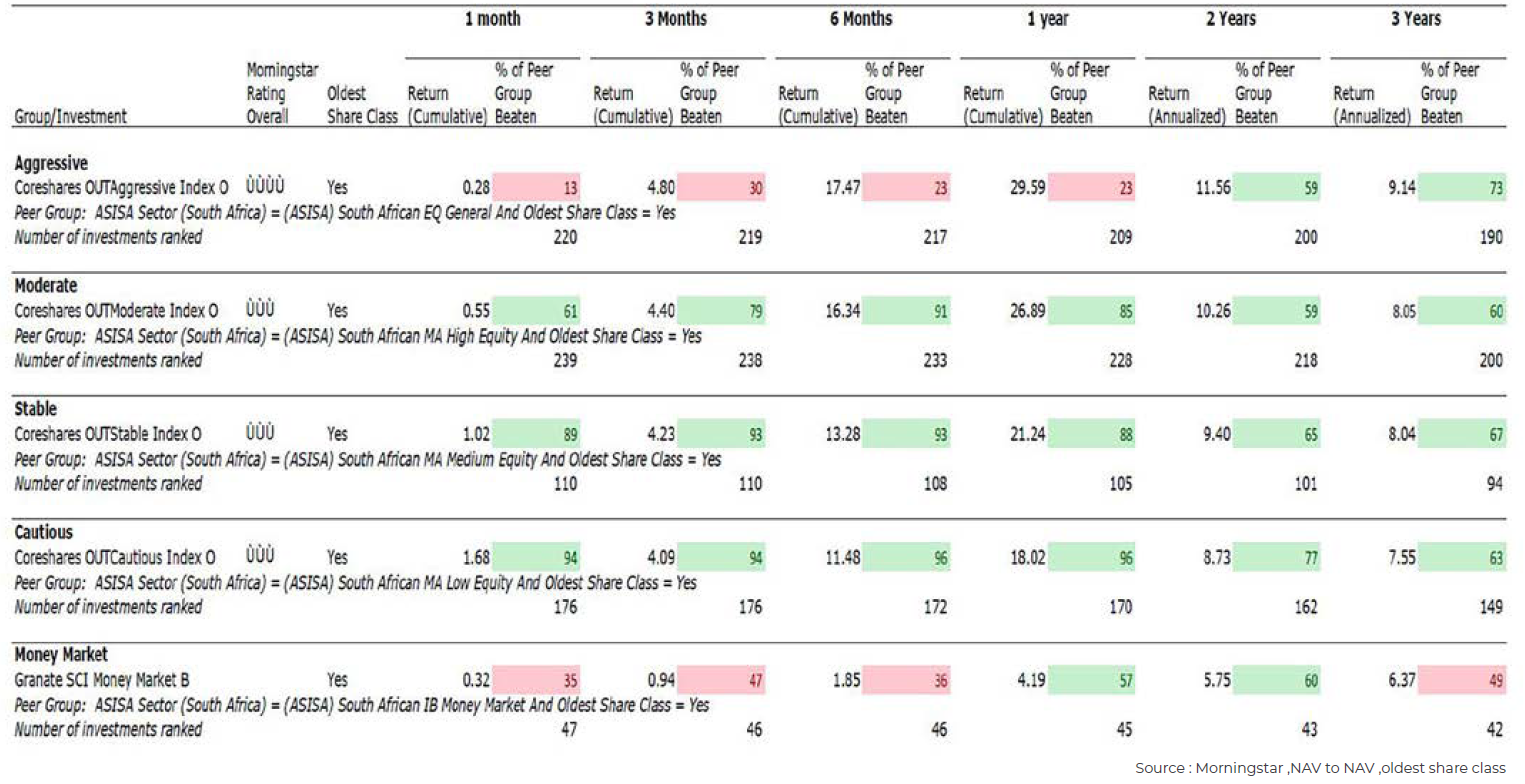

OUT funds performed satisfactory in May, with 3 out of 5 funds beating more than 50% of the peers in their peer group.

The CoreShares OUTaggressive Index fund performed poorly when compared to its peers in the month of May, the fund only managed to beat 13% of its peers in May, however the fund performed extremely well in absolute terms on a 1 year basis ending May, the fund gave investors more than 29% in gains in the past year.

The CoreShares OUTmoderate index fund had a satisfactory May, the fund managed to beat 61% of funds in the same ASISA category. Over the past year the OUTmoderate fund managed to outperform 85% its peers.

The CoreShares OUTstable fund had a spectacular May, the fund managed to beat 89% of its peers, the fund returned 21.24% for the year ending May 31st.

Over the past 3 years the OUTstable fund has given investors just over 8% on an annualized basis.

The CoreShares OUTcautious Index was the best performing fund both in relative and absolute terms, the fund managed to beat 94% of its peers and returned gains of 1.68% to investors.

The fund returned more than 18% to investors for the year ending May 31st. The OUTcautious fund has returned an average of above 8 % in the past 2 years