With the 2020 State of the Nation Address (SONA) behind us, there are distinct camps in South Africa right now: The pessimists and the quiet optimists who are starting to see signs that the country is moving in the right direction.

The OUTvest investment committee recently met to debate the outlook for the next quarter and we can firmly say that we sit in the second camp.

One of the key themes was that we spend too much time focusing on the mining and industrial sides of the South African economy and are missing some of the good work being done in other key sectors.

The committee pointed out recent insights shared by JP Landman which pointed to policy clarity in the financial services sector, key decisions taken in the telecoms sector and some encouraging data coming out of the tourism and agriculture sectors.

The automotive sector was identified as one where there was also some good news with significant new investment activity and an increase in the number of cars sold into the export market.

On top of this, government appears to have softened its stance around allowing energy-intensive mining companies to generate their own power. This announcement at the 2020 Mining Indaba was welcomed as a great way to reduce the strain on the electricity grid.

This is supplemented by the announcement in the SONA that The National Energy Regulator will ensure that all applications by commercial and industrial users to produce electricity for own use above 1MW are processed within the prescribed 120 days.

Just this week, StatsSA released employment data for the last quarter which included two interesting points which tie into the view of the investment committee:

- South Africa’s primary agriculture sector saw a 4.2% (36 000 jobs) increase in employment.

- The last quarter of 2019 was the first time that the unemployment rate had not risen since 2008.

While a lot more needs to be done, there are some signs that we are seeing some turning points in terms of activities to stimulate the South African economy.

For the 12 months ended 31 December 2019:

- The All Share Index returned 12% largely driven by 28.5% return in the resources sector

- The JSE Mid-Cap index returned a solid 15%

- On the global front, the S&P500 returned 27.8% in rand terms

- Listed property was again the laggard on the local front, returning just 1.9% compared to the S&P Global Property Index which rose 19.5% over the same period in rand terms.

Source: Thomson Reuters Datastream, all figures quoted over 1 year to 31 December 2019

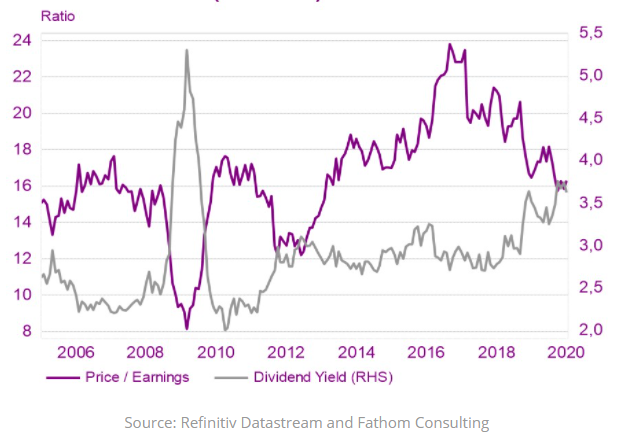

The investment committee were unanimous in their view that South African markets are cheap on a number of metrics and that any good news on the economic front could drive a move to the upside.

The below graph reinforces this view showing rising dividend yields and undemanding price to earnings multiples on JSE (Johannesburg Stock Exchange) listed businesses:

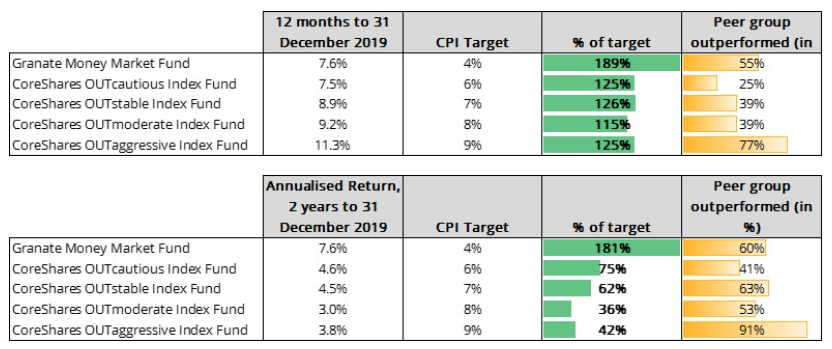

How did the funds perform last year?

Astute investors will have noticed that the value of their investment fell sharply on the 24th of February as a result of global investors moving to safer assets over fears the impact Corona virus (COVID-19). The JSE Top 40 Index (SA Equities) fell by nearly 4.5% and the S&P 500 Index (US Equities) fell by 3.3% on the 24th of February. The fund values fell by between 3.5% for the CoreShares OUTaggressive to 1.3% for the CoreShares OUTCautious, and 0% for the Granate Money Market Fund on the same day. We remind our valued clients that we don't react to short term price changes, we believe remaining invested in the markets as we believe that short term market timing is incredibly difficult to predict and trade around.

Over the last year the funds performed well against their inflation targets but struggled against their peers due in part to the allocations to index-linked bonds, which have not performed as well as cash and nominal bonds. As always, you need to be aware that your investment returns will differ from those shown below because your investment will occur at different times. In technical terms, it's the difference between a time-weighted and a money-weighted return. Most client's experience a money-weighted return (the amount and timing of your investment influences your returns), but investment managers want to ignore the impact of investor cash flows in their investment returns and so report using a time-weighted return.

Source: Morningstar and Thomson Reuters for CPI information. CPI target is the nearest annualized 1 and 2 year CPI (Consumer Price Inflation) calculated to December 2019. Fund information is net of management fees and calculated using NAV. Past performance is no guarantee of future returns.

We use the ASISA SA Equity General as a representative peer group for the CoreShares OUTaggressive Index Fund rather than the ASISA Worldwide Equity General - the peer group on the trust deed as we feel it is more relevant based on the asset allocation. Past performance is not indicative of future performance, not guaranteed and dependent on the performance of the underlying investments

A key question that has been asked of the OUTvest team was whether the South African market was open to a robo-advisor solution and would embrace technology as part of their saving journey.

The launch of our ONEfee and Retirement Annuity solutions have been game-changers and we were pleased to report a record in-flow during January 2020 for OUTvest as South Africans embraced the use of our low-cost, efficient solutions for building wealth.