Similar with investing, a proper understanding of your investment time horizon, asset allocation and fee structure can either make or break your financial plan, and not necessarily how many times you try time investment markets.

Things like political instability, economic shocks, and even global pandemics cause great discomfort, fear and uncertainty for investors.

Yet these factors come and go over time and are less important in the scheme of things when your focus is on the end goal and not the short term “noise”.

We firmly believe in following an outcomes based investment philosophy underpinned by a solid understanding of your time horizon, asset allocation and fees.

A good starting point before selecting any investment product or investment vehicle is to define and understand your investment time horizon.

Defining your investment time horizon is easy, sticking to it is the real challenge.

If you are saving for a holiday in four years’ time you have a four year investment time horizon. If you are saving for retirement twenty years away you have a twenty year time horizon. It’s that simple.

So why is defining your time horizon so important? Your time horizon is a key driver in determining the most appropriate investment product or vehicle to help you achieve your desired investment outcome.

If you chose a twenty year investment time horizon you should generally have a different investment product or vehicle to those that chose a four year investment time horizon.

Different investments products have unique risks and returns assumptions that ultimately deliver different investment outcomes and expectations.

Defining your investment time horizon (and committing to it) is probably the most important step when it comes to choosing an investment.

So often investors love to compare their investments with those of their peers or other service providers, yet often do so incorrectly, as they focus on the performance of their investment as a driver instead of the time horizon.

Consider the following:

Mrs. X invested in an investment with a time horizon of one year and earned a 6% return after one year. Mr. Y invested in an investment with a time horizon of twenty years and received a 2% return after one year.

Off the bat it would appear that the 2% return was a “poor investment” choice, however these two investments are not comparable over a one year period as their investment time horizon differs.

Both these investments have fundamentally different investment risks designed to achieve different outcomes after a predetermined period of time.

The “2% investment” still has another nineteen years to go, while the “6% investment” has achieved its one year time horizon outcome.

Only after nineteen years can one then properly compare these two investments to determine which one was actually better.

It is a little like trying to compare a sports car with an off–road SUV. They are both cars, yes, but have very different objectives and built to achieve very different outcomes. Hence comparing them is not wise.

Comparing sports cars with sports cars is more prudent and meaningful, same as investing, comparing investments with similar time horizon investments is meaningful and prudent as they are chasing a similar outcome and have a similar “build”.

Once your time horizon has been clearly defined the next important step is selecting an appropriate asset allocation to match.

Asset Allocation is basically the way that your money will be invested between various asset classes (cash, bonds, property, equities (shares in companies), etc.) over time to try achieve a certain growth outcome.

Asset allocation is like the engine in cars. A sports car will have a more aggressive engine designed for speed and power, while the off-road SUV will have an engine designed for torque to literally climb mountains.

If you place a sports car engine in an SUV you will probably burn it out and have endless issues as your objective of bashing through the bush might not be achieved.

When travelling through the bush speed is not required, strength and torque are key. Hence the right engine in the right vehicle is important to achieve the desired outcome.

Investing is similar, when investing for the short term a conservative asset allocation (low risk engine) is prudent, as time is against you. While investing for the long term a more aggressive asset allocation (higher risk engine) is prudent as time is on your side.

Over time investment markets will fluctuate (go up and down) unpredictably however with time on your side you can take advantage of more good times which can offset the bad times.

If time is not on your side then the risk of not recovering from the bad times is greater.

If you are investing for a one year period you would want to remove as much risk and uncertainty as possible to try protect your capital.

Normally that would mean avoiding high risk investments like equities (shares in companies) and rather invest in low risk options like cash or bonds.

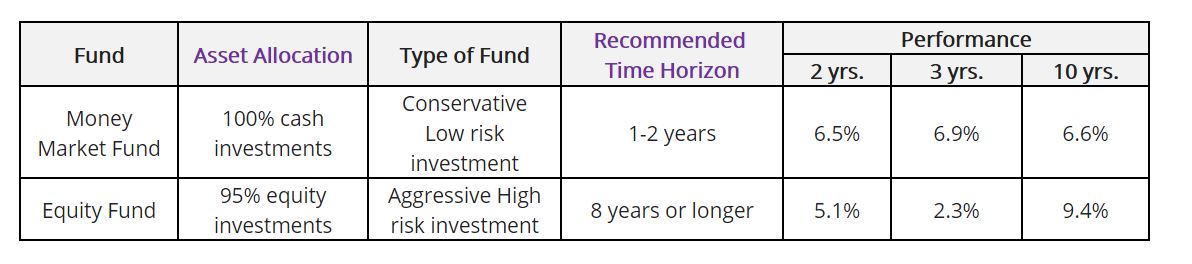

Consider the following table showing the performance of a certain asset managers’ funds over a 2, 3 and 10 year period.

What is noticeable is that the cash fund (MM) returned a rather consistent growth over the various time periods.

The reason for this is that the “cash asset class” has a very low risk and not subject to big market movements like equities (shares in companies) over time.

The equity fund on the other hand was extremely volatile over the short term but over the long term outperformed the cash fund.

The reason for this is that the equity asset class generally delivers long term growth despite some very poor short term growth periods.

What is important is that these funds should not be compared with each other as they have different recommend time horizons with different asset allocations designed to achieve different investment outcomes.

So effectively each fund did their job in relation to their respective recommended investment time horizons.-

The longer term investor wanted a higher outcome and was prepared to accept the short term noise and lack of performance, whereas the short term investor could not afford to have any bad or low performance like the 2.3% generated by the equity fund after 2 years.

In fact during the long term investors’ journey there was a point where he must have felt frustrated and possibly lost confidence in the equity fund after only achieving a 2.3% growth after 2 years.

However 2 years was not the end goal but rather 10 years (as per the fund’s recommended investment time horizon). So by sticking to the 10 year time horizon and staying invested he was rewarded as the fund’s asset allocation did deliver handsomely over the long term.

As a general investment principle: The longer an investment time horizon the more the associated risk (greater asset allocation to equities and high risk investments) but with a greater potential for better growth, than short term investing.

Investing generally “goes wrong” for investors when they don’t stick to their time horizon and select the wrong asset allocation to match. It’s like trying to ride the sports car through the bush or trying to place a sports car engine in the off-road SUV.

Everything just does not fit and the ride is extremely unpleasant not to mention uncertain!

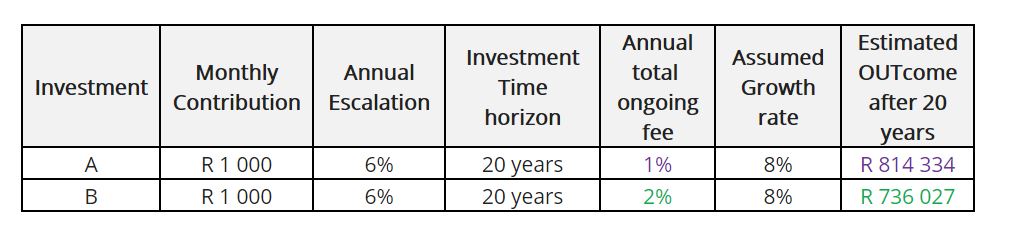

Finally, considering all fees applicable to an investment is critical as fees can have a fundamental effect on your investment outcome over time.

Even a 1% fee difference sounds insignificant yet over long periods of time a 1% fee saving can have a major impact.

The table below shows the difference that a 1% fee saving can have on an investment of 20 years.

Before committing to any investment it is sensible to understand all the fees that apply as every cent counts. The more you save in fees the greater your potential investment growth.

A useful way of comparing fees charged by various service providers is to ask each for their Effective Annual Charge (EAC) statement.

Once you have the various EAC statements you will have a good idea as to how much it costs you to invest with a particular provider.

The investment journey can either be a nightmare or dream and it really depends on a proper understanding of the importance of your investment time horizon, asset allocation and fees.

There are other aspects that also need consideration when investing but understanding these three creates a solid investment foundation with better investment expectations.