In a previous article entitled “Did You Know: SARS is also a “Giver of Revenue” we shared five useful “did you know facts” as to how SARS’ tax incentives can help grow your wealth. In this article, using the abovementioned article as a basis, we explore a practical example as to how these tax incentives can be used smartly to give your financial plan a solid boost.

Please note that this example does not constitute financial advice and does not take into account one’s personal financial circumstances. It is merely for illustrative purposes to highlight ways as to how investors can take advantage of some of SARS’ tax incentives to enhance investment outcomes.

Joe’s Financial Position

Joe Soap, a 30 year old male, earns a company salary of R400 000 per annum. He does not belong to a company retirement fund and must make his own provision for retirement. Joe has R1 500 pm available to invest towards his retirement till age 65.

Joe has recently inherited R1 000 000 cash from a distant family member and was wondering how to best invest this tax efficiently. He intends to invest until age 65 to supplement his retirement.

Joe has no other investments or income for purposes of this example.

Some Investment Considerations for Joe

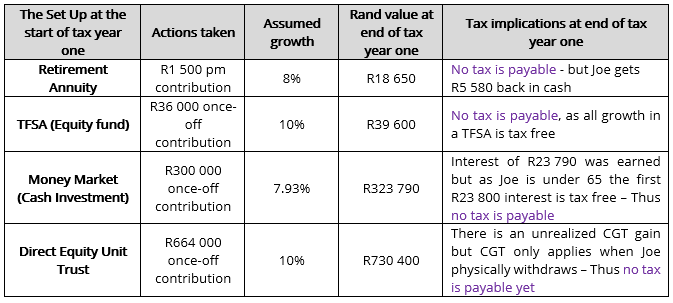

A Retirement Annuity Investment

Joe can open a Retirement Annuity (RA) in order to provide for his retirement whilst also taking advantage of lowering his SARS tax liability every year while contributing. SARS allows contributions of up to 27,5% of your taxable income (capped at R350 000) per annum to be deducted from your taxable income. He indicated that he has R1 500 pm available to invest for retirement.

If Joe opens and contributes R1 500 pm towards a retirement annuity, using the 2023/2024 tax tables published by SARS, Joe could get R5 580 back in cash from SARS.

Splitting the R1 000 000

Joe can consider splitting his R1 000 000 inheritance as follows to take further advantage of some of the SARS tax incentives:

- A Tax Free Savings Investment

He takes R36 000 and opens a Tax Free Savings Account (TFSA) Investment. In a tax year the most an investor can contribute to a TFSA is R36 000. He invests in an aggressive equity unit trust within the TFSA chasing long-term growth while accepting short-term fluctuations.

- Cash Investment

He invests R300 000 in a Money Market Investment (cash investment) where he earns 7.93% interest per annum.

- A Direct Equity Unit Trust

Joe invests the balance of R664 000 into a direct equity unit trust. This unit trust invests completely in shares listed on the Johannesburg Stock Exchange (JSE), with short-term volatility and fluctuations but with greater longer-term expected investment returns.

All growth in this direct equity unit trust is subject to Capital Gains Tax (CGT). However CGT only applies when Joe withdraws from the investment. We assume Joe has no other investments attracting CGT.

The Set Up

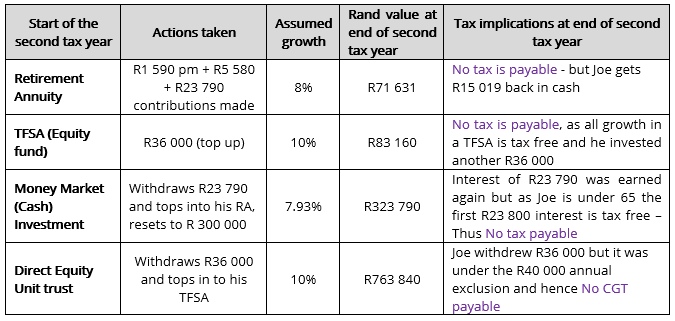

At the start of the second tax year…..

Joe makes the following nifty tax moves

For purpose of this example we assume the SARS tax rates and incentives remain unchanged.

- He withdraws R36 000 from the Direct Equity Unit Trust and adds this to his TFSA. No tax applies to the withdrawal as the R36 000 is less than the R40 000 annual CGT exclusion.

- He invests the R5 580 cash received from SARS back into his RA.

- He wisely increases his RA contributions by 6% to keep up with inflation. His salary also increased by 6% to R424 000.

- He estimates that his cash investment should again grow by 7.93% this tax year. To avoid exceeding the R23 800 tax interest exemption Joe withdraws R23 790 from this investment and adds this to his RA.

At the end of the second tax year….

At the end of the second tax year, assuming the tax rates remain unchanged, Joe could get back a whopping R15 019 from SARS. This was based on his new salary of R424 000, the adjusted monthly contributions of R1 590 as well as the two additional contributions of R5 580 and R23 790 respectively that Joe made to his RA.

His investment position at the end of the second tax year:

Joe used the tax free money generated through the tax incentives (R5 580 and R23 790) to boost his RA and in the process got even more money back from SARS. All growth in the RA is tax free with the added bonus of getting cash back each tax year.

By topping up his TFSA from the direct equity unit trust (R36 000), he converted money that would have been subject to CGT to tax free money.

Joe never paid any tax on his investments in these two tax years. He cleverly used the tax incentives to invest tax free and then moved this “tax free money” to boost his investments and generated even more tax free returns.

At the start of every tax year Joe follows a similar tax harvesting exercise to ensure that his portfolio is tax efficient and working for him – largely thanks to the annual SARS tax incentives.

Gareth van Deventer CFP®