Alexforbes acquires OUTvest

![]()

Alexforbes has acquired 100% of the shares in OUTvest, and we are proud to be a part of this leading South African financial services group.

Grow your preservation fund

A preservation fund is a tax-efficient way to ensure that your hard-earned money goes towards your retirement.

When you invest in an OUTvest preservation fund, you're essentially giving yourself a way to preserve the value of a lump-sum amount. And thanks to our revolutionarily low fees, your lump-sum amount is more likely to grow at the best possible rate.

Transfer your pension or provident fund to an OUTvest preservation pension fund

If you've been retrenched, dismissed, or you've resigned from your job, you may be wondering what to do with the pension or provident fund you had with your previous employer.

It might be tempting to cash out the funds so that you have some extra cash in your day-to-day life. But transferring the funds to an OUTvest preservation fund is a great way to ensure the money goes towards your long-term, retirement goals.

Thanks to our low-fee advantage, you'll preserve your savings more effectively so that you get more OUT at retirement, and you'll also keep the tax benefits attached to your provident or pension fund. In short, your future self will thank you!

Transfer my pension/provident fundSwitch your current preservation fund to OUTvest

If you already have a retirement preservation fund, consider switching it to OUTvest. Thanks to our industry-first fees structure, you might find that you spend significantly less on preservation fund fees, which helps you to build your wealth in the long-term.

Why should you preserve your investments with OUTvest?

Why should you preserve your investments with OUTvest?

How our ONEfee model boosts your preservation fund

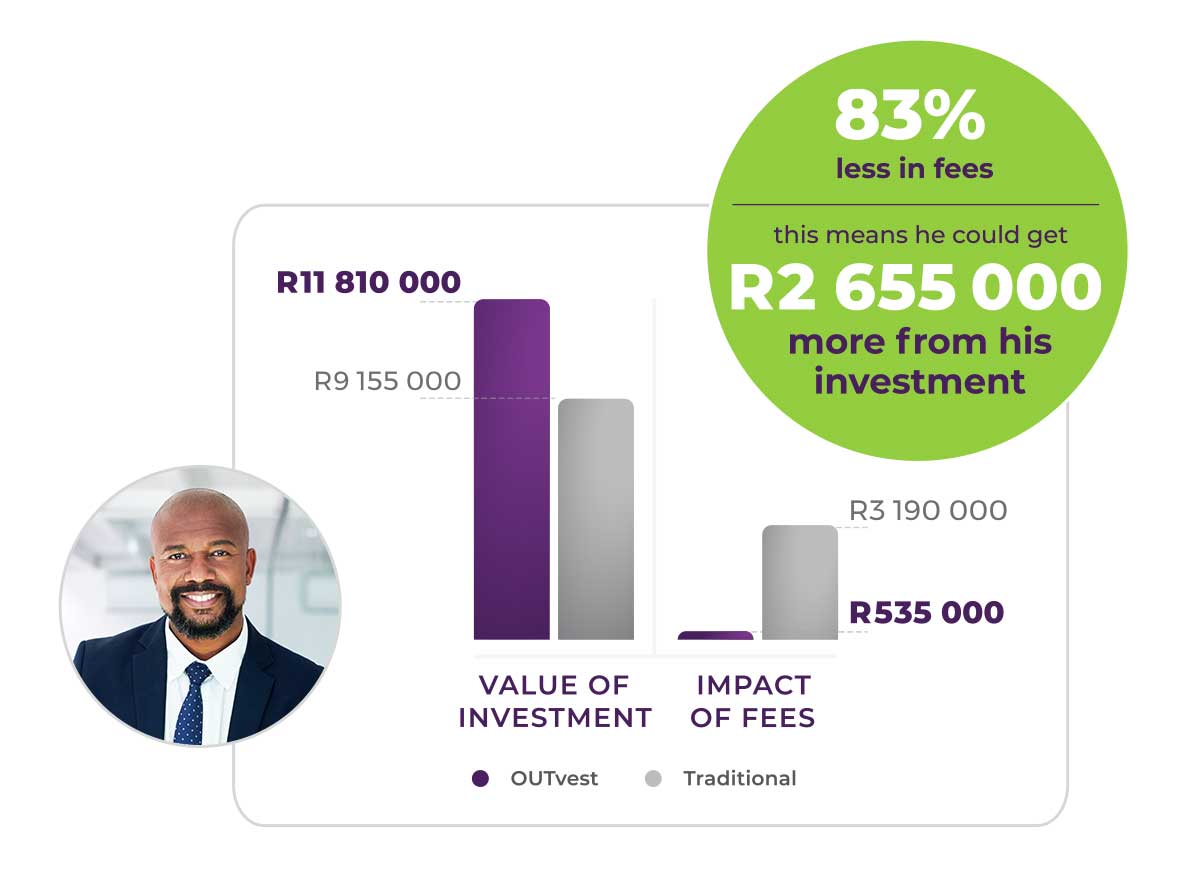

Joseph, aged 45, had R500 000 in his pension fund. When he resigned, he decided to transfer that money into an OUTvest preservation pension fund for the next 10 years.

Thanks to our ONEfee model, Joseph saved 83% in preservation fund fees. This means he could get up to R2 655 000 more OUT at retirement.

Learn more about ONEfee Switch my preservation fund to OUTvestProfiles used are only for illustrative purposes. The total cost of “Traditional investing” is estimated to be 3% per year. Traditional investing is when you pay an advice, administration and fund management fee. The results are modelled based on a historical growth rate using the asset allocation of the CoreSolutions OUTmoderate fund. Research on fees was conducted by OUTvest internally. Past performance is not indicative of future performance. All investments are exposed to risk, not guaranteed and dependent on the performance of the underlying investments and excludes the impact of Securities Transfer Tax. Fees may change due to inflation.

Frequently Asked Questions

Can I make contributions to a preservation fund?

By law, you can't make any additional monthly or lump sum contributions once you have invested in a preservation fund. You can only transfer money from a pension, provident or another preservation fund to a preservation fund.

Can I withdraw from a preservation fund? What are the withdrawal rules?

Preservation funds differ from Retirement Annuities in that you can withdraw from them any time before the age of 55. But bear in mind that the withdrawal is subject to taxation and can only be done once in your lifetime.

If you've already taken money from your retirement fund before you transfer to a preservation fund you might not be eligible to make a withdrawal.

When can I retire from my fund?

You can retire from your preservation fund any time after the age of 55. But you need to consider that there might be certain tax implications when you retire from the fund.

At retirement, for any non-vested benefits in a preservation fund, you are allowed to access up to 1/3rd of the funds in cash, subject to taxation, while the remaining portion must be used to purchase an income for life (Living annuity or guaranteed annuity). If your fund value is less than R 247 500 when you retire, you can access the full amount in cash, subject to taxation.

For any provident or pension preservation fund vested benefits at retirement, you can take the full benefit as a lump sum, or take a portion of the benefit as a lump sum and use the remaining amount to purchase an income for life (living annuity or guaranteed annuity).

What is the minimum amount I can transfer?

We will accept transfers for amounts of R 25 000 and more.

Can I transfer my other retirement preservation fund to an OUTvest preservation fund?

Yes, and we can assist you with the process. The best part is that this transfer is done tax-free. Due to the number of parties involved in the process, these kinds of transfers can take some time. But not to worry, we will help you every step of the way.

What happens to my OUTvest preservation fund if I die?

A board of trustees is responsible for running the Preservation fund and protecting the interests of all members. If you die while still invested in the OUTvest Preservation fund the trustees must trace those that are financially dependent on you and allocate the funds appropriately.

Is the OUTvest preservation fund protected from my creditors?

Yes, once your money is invested in the OUTvest preservation fund it is protected from all your creditors, thus ensuring you have something to help you retire with one day, even if you were sequestrated.

What is a vested and a non-vested benefit?

Vested benefits are accrued rights as a result of any membership in a provident fund or provident preservation fund on 1 March 2021. If you have been a member of these funds at the time, any amounts contributed or transferred to these funds, before 1 March 2021, are seen as your vested benefits.

If you were 55 years or older on 1 March 2021, your vested benefits will also include any further contributions you made while you were a member of that provident fund, including fund returns. A vested benefit right gives you the right to be able to withdraw the full benefit value as a lump sum upon retirement.

Non-vested benefits relate to any other benefits in a retirement fund, which gives you the right to be able to only withdraw up to a maximum of 1/3rd at retirement. The remaining portion of the non-vested benefit must be used to purchase an income for life (Living annuity or guaranteed annuity) at retirement.

Can I withdraw my preservation fund if I emigrate?

Recent legislation stipulates that you can withdraw your preservation fund under the following conditions:

-If you have emigrated from South Africa and your emigration is recognised by the South African Reserve Bank for purposes of exchange control. This is in respect of applications for that recognition received on or before 28 February 2021 and approved by the South African Reserve Bank or an authorised dealer in foreign exchange for the delivery of currency on or before 28 February 2022.

-If you leave South Africa at the end of a work visa or visitor’s visa, as contemplated in the Immigration Act of 2002, subject to the deduction of income tax on the amount, as provided in the Income Tax Act.

-If you are a person who is not a resident for an uninterrupted period of three years or longer on or after 1 March 2021. (But bear in mind that if you're under the age of 55 you don't need to wait 3 years or longer. You can make a full withdrawal from your preservation fund at any time, subject to taxation).