Your investment funds

In our last report covering the first three months of 2018 we saw negative returns on every fund except the Granate Money Market Fund.

The good news is that over the past three months (to the end of June 2018) we have seen a recovery and all the funds have delivered positive returns - enough to cover the losses of the first quarter and then some. This means, overall, we’re in positive territory for the first six months of 2018.

The value of your investments changes every day, going up and down based on the performances of the shares, bonds, cash and property investments in the unit trust in which you are invested.

Most of our OUTvestors have monthly recurring investments, and as such are taking excellent advantage of a powerful method of investing known as rand cost averaging. It’s a great way to get into the investment markets.

Our investment committee regularly evaluates the performance of the investment funds we us. We compare the performance of the funds against their peers as well as the indices that we have developed in-house, in conjunction with CoreShares.

We remain happy with the performance of all the funds, both against their peers and the indices.

Speak to one of our financial advisors and start your investment journey.

Twenty-eighteen started with a party! Consumer confidence in the South African economy took off like a rocket, the Rand strengthened to R12 against the US Dollar and South African companies listed on our stock exchange, the JSE, rose as investors bought shares in our companies.

We even avoided a complete downgrade of our country's debt to junk status. Our new/old finance minister, the wonderful Mr Nhlanahla Nene, believed that economic growth would be above expectations.

All of this took place mainly thanks to the astounding political movements within the ANC. So far President Cyril Ramaphosa has delivered on his promises, the boards of Eskom, Denel, Prasa and more have been replaced and these entities are recovering – now overseen by the indomitable Pravin Gordhan.

The mining charter is finally moving again, thanks in major part to the new Mineral Resources Minister, Gwede Mantashe. By the way, has anyone heard from the Gupta’s recently?

And then…came the news that economy actually shrank between March 2017 and March 2018 and markets suddenly went into reverse and our currency weakened significantly.

What on earth happened?

Well, it isn’t simple. Firstly, it’s not all South Africa’s fault. Donald Trump decided to fulfil his election promises and has started to introduce tariffs on certain items imported into the US. He is doing this to protect American companies, and therefore American jobs. China is extremely upset and is threatening to retaliate.

There is a saying: “When elephants fight, it is the grass that suffers.” South Africa (the grass J) is caught up in this tussle as our steel and aluminium exports to the US will be subject to tariffs, making them more expensive in the US and affecting South African jobs.

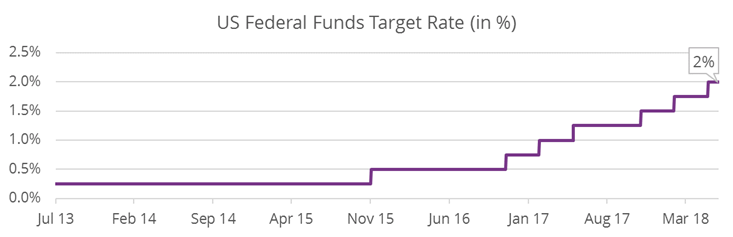

Secondly, US economic growth has been strong and inflation is rising. As a result the US Federal Reserve (effectively the same as the South African Reserve Bank) is raising interest rates.

Foreign investors are starting to move money from emerging markets like Brazil, China, India and of course, South Africa, back to the US because the US interest rates are starting to offer a reasonable return for the risk.

Take a look at the chart below to see how US rates have been rising over the past few years.

Source: Thomson Reuters / Fathom Consulting – to end June 2018

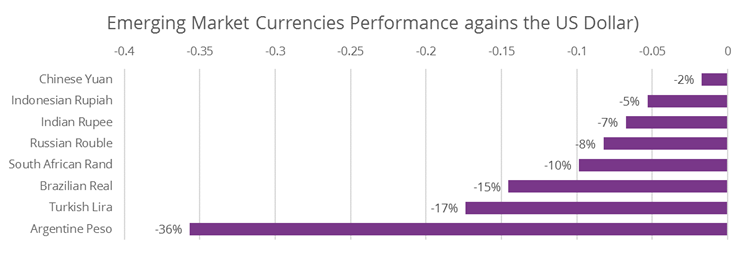

In addition our currency isn’t the only one suffering at the moment. The chart below shows the performance of other emerging market economies compared to the US dollar as a result of investors moving money back to the US.

Source: Thomson Reuters Datastream / Fathom Consulting, data to end June 2018

However, South Africa must also accept its share of the blame. Let’s say that at the party in January everyone had a little too much to drink. We woke up in April, with a hangover, to the reality that not much has changed.

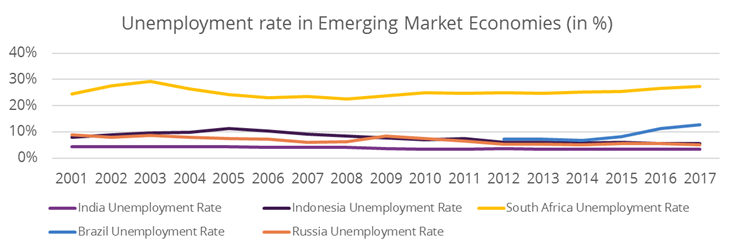

The structural problems in the South African economy, including primary education, unemployment and inequality, are still with us, and will be for a long time. The chart below gives an indication of our unemployment rate as compared to other emerging market economies, just to give you an idea of the scale of the problem – our unemployment is way higher.

Source: Thomson Reuters Datastream / Fathom Consulting to end 2017

Lastly - Don’t forget that 2019 is an election year and politics is dominating conversations across South Africa. From land reform to mining reform to radical economic transformation, these are huge issues that need dealing with if South Africa is to progress economically and politically.

I see this as a positive step in South Africa’s future. The dialogue is open and in the public domain, and the governing party is taking measured steps to achieve its mandate while managing the stability of South Africa, politically and economically.

The markets

Here’s how some of the key investments in our unit trusts performed:

South African equities: Over the first three months of 2018 the largest 40 shares on the Johannesburg Stock Exchange (JSE) had fallen 6%. From March to the end of June, the same 40 shares were up 6% again, mostly driven by growth in companies in the natural resources sector.

South African listed property: This sector fell a further 2% from March to June, partly as a result of investors trying to understand some potentially creative and confusing accounting in one of the largest listed property companies, namely Resilient.

US equities: Over the three months to the end of June, the US equities (shares) were up by more than 3%. However, in South African Rand terms the performance was close to 20% - an indication of just how volatile (fluctuating) our currency is.

Emerging market equities: In the second quarter of 2018, the performance of emerging markets was actually negative, down close to 3%, but as per US Equities the performance over the quarter from the perspective of a South African investor was actually over 7%.

South African bonds (loans to the South African government): Bonds actually delivered negative returns during this period as foreign investors moved money out of South Africa to the US.

Data provided above was sourced from Thomson Reuters Datastream and calculated by OUTvest. Data to end June 2018.

The performance of our unit trusts.

The performance numbers provided below have been sourced from Morningstar, a leading fund information service provider.

Broadly speaking we are happy with these numbers, especially when measured against our industry peers. The figures below show how our funds performed between January and June 2018:

|

Fund |

3 month return |

6 month return |

1 year return |

|

Granate Money Market Fund |

1.9% |

3.7% |

7.7% |

|

CoreShares OUTcautious Index Fund |

1.0% |

2.0% |

7.9% |

|

CoreShares OUTstable Index Fund |

3.2% |

1.9% |

9.2% |

|

CoreShares OUTmoderate Index Fund |

5.4% |

1.2% |

11.7% |

|

CoreShares OUTaggressive Index Fund |

7.3% |

1.9% |

13.3% |

Source: Morningstar, sourced by CoreShares Asset Management on behalf of OUTvest (Pty) Ltd. Past performance is no guarantee of future returns.