Retirement does not necessarily mean waiting to be “old and grey” it simply means choosing not to work and being able to support your lifestyle with the funds you have put in place for this purpose. There is no perfect recipe when it comes to retirement funding as it is entirely up to each individual as to how they will go about preparing financially for their retirement.

Retirement funding essentially encompasses two phases, the accumulation phase and the drawdown phase. In the accumulation phase investors are largely investing money for the long-term without touching a cent until retirement. In the drawdown phase investors start drawing an income from the money they saved up during the accumulation years. Each phase requires a solid investment strategy with investment products to match.

The good news is that there are excellent investment products tailored specifically to match most investor’s retirement needs during both phases of retirement funding. Before deciding how to fund your retirement it is best to understand the various product options available in the South African market designed exclusively to fund both phases of retirement.

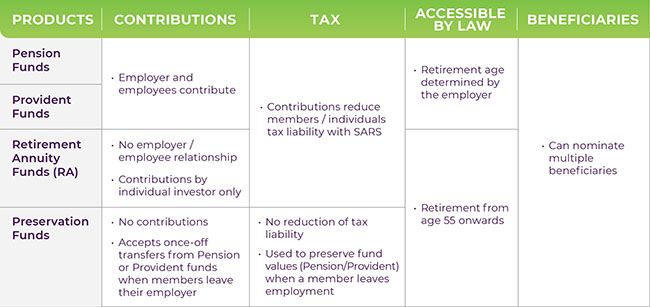

Accumulation Phase Options

A pension and provident fund is offered by an employer and employees must belong to the fund as per the conditions of their employment. Employees are limited in terms of investment choice and fees as employers decide which retirement funds to implement.

In a retirement annuity (RA) and preservation fund the individual and not the company can determine the choice of investment funds and fees, as there is no employer / employee relationship. Members of RAs and preservation funds thus have more choice than members of employer funds (Pension and Provident).

Being a member of a company’s retirement fund and supplementing this with a retirement annuity is a smart retirement funding strategy.

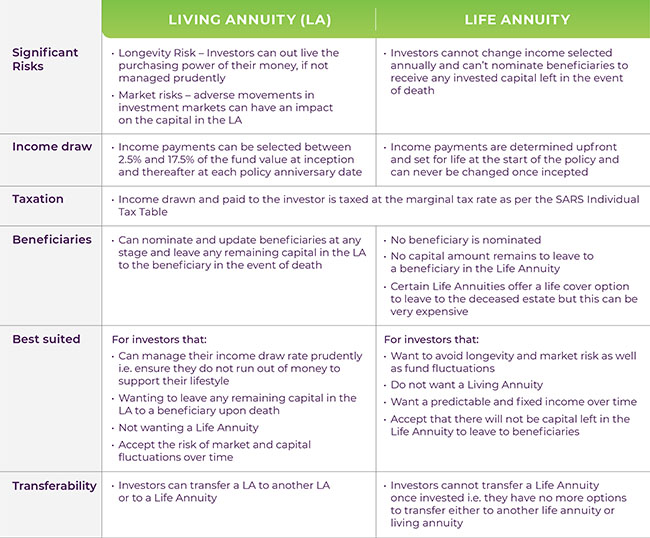

Drawdown Phase Options

When reaching the respective retirement ages applicable to various retirement funds in the accumulation phase, investors have the following options (products) to provide them with an income in the drawdown phase:

![]()

It is important to note that an investor will need to exit their specific retirement fund in the accumulation phase and transfer their funds over to either a life, living annuity or a combination in order to receive an income.

Some differences between a living and life annuity:

Supplementary Products to boost Retirement Funding

Besides the products mentioned in both phases other investments like Tax Free Savings Investments (TFSA), direct unit trusts and endowments can also be used to boost retirement funding. A TFSA is especially tax advantageous when used in conjunction with a retirement annuity as part of a solid retirement funding strategy.

There are excellent retirement funding options available in the South African market to help investors live their best life and seeking proper financial advice is crucial.